What is a kids portfolio? And why is it worth it?

A kids portfolio is a securities portfolio specifically designed to build long-term wealth for children. Instead of simply parking money in a bank account, it is invested in assets such as stocks, gold, or real estate. The goal is to create a solid financial cushion over the years, whether for a driver’s license, a first apartment, or as starting capital for adult life.

The invested money is broadly diversified via index funds and can thus benefit from the development of global financial markets.

In contrast, classic savings accounts in Switzerland today yield almost no interest. In recent years, the interest rate was not even sufficient to compensate for inflation. The assets lose purchasing power.

Over a horizon of 40 years, inflation can eat away about half of the assets. Thinking about the returns that could have been earned during this time if the money had been invested can be quite painful.

Savings Account vs. Kids Portfolio: Which is more worthwhile?

A historical comparison clearly shows the differences between a savings account and a kids portfolio:

In 2008, your child is born and you make a one-time transfer of CHF 10’000 to a savings account and a one-time transfer of CHF 10’000 to a VIAC Invest kids portfolio with the Global 100 strategy. For the savings account, we assume an annual interest rate of 0.5%, while we use historical price data for the kids portfolio.*

Your child is to receive the entire amount on their 18th birthday.

*For historical values until December 2024, comparable price data for the Global 100 strategy is used.

After 18 years, your child would have an amount of CHF 10’939.29 in the savings account, while the amount in the kids portfolio would be more than twice as high at CHF 25’399.63. Since the interest on the savings account could not compensate for inflation, the money parked there has effectively lost value over the years, and you can afford less with that money than at the time of your deposit.

If the child were to leave the money invested or in the savings account for another 7 years, they would have an amount of CHF 54’175.59 in the kids portfolio and CHF 11’672.07 in the savings account at age 30, assuming an average return of 6%.

A child’s long investment horizon is ideal for investing in securities. Due to the many years until the money is used, short-term market fluctuations can be weathered, while the compound interest effect can unfold its full impact: earnings are reinvested, allowing assets to grow increasingly faster.

In our example above, the amount is invested shortly before the 2008 global economic crisis and subsequently loses almost half of its value. This is another example of how important a long investment duration is, as the money remains invested and not only recovers but gains significant value in the long term.

Why is a long investment duration such a great advantage?

The following comparison impressively shows what a long investment duration makes:

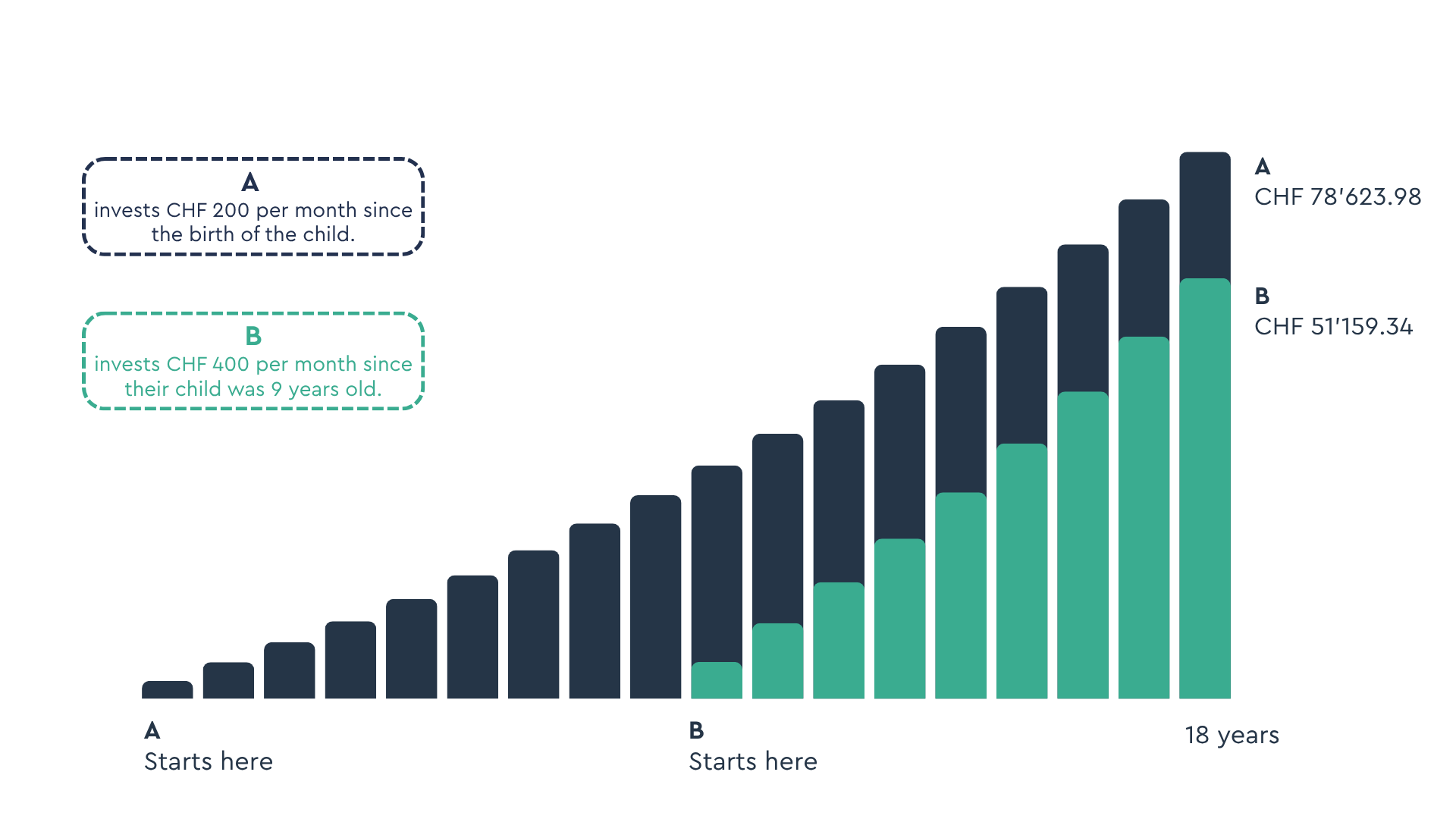

Person A set up a portfolio for their child at birth and invests CHF 200 monthly (CHF 2’400/year). Person B only started when their child was 9 years old, but invests CHF 400 per month (CHF 4’800/year).

By the time their children turn 18, both persons have invested the same amount of CHF 43’200. For the comparison, we assume an average return of 6% per year.

The result: Person A’s child receives CHF 78’623.98 on their 18th birthday, while Person B’s child receives only CHF 51’159.34. That is a full CHF 27’464.64 less, even though the same amount was invested for both.

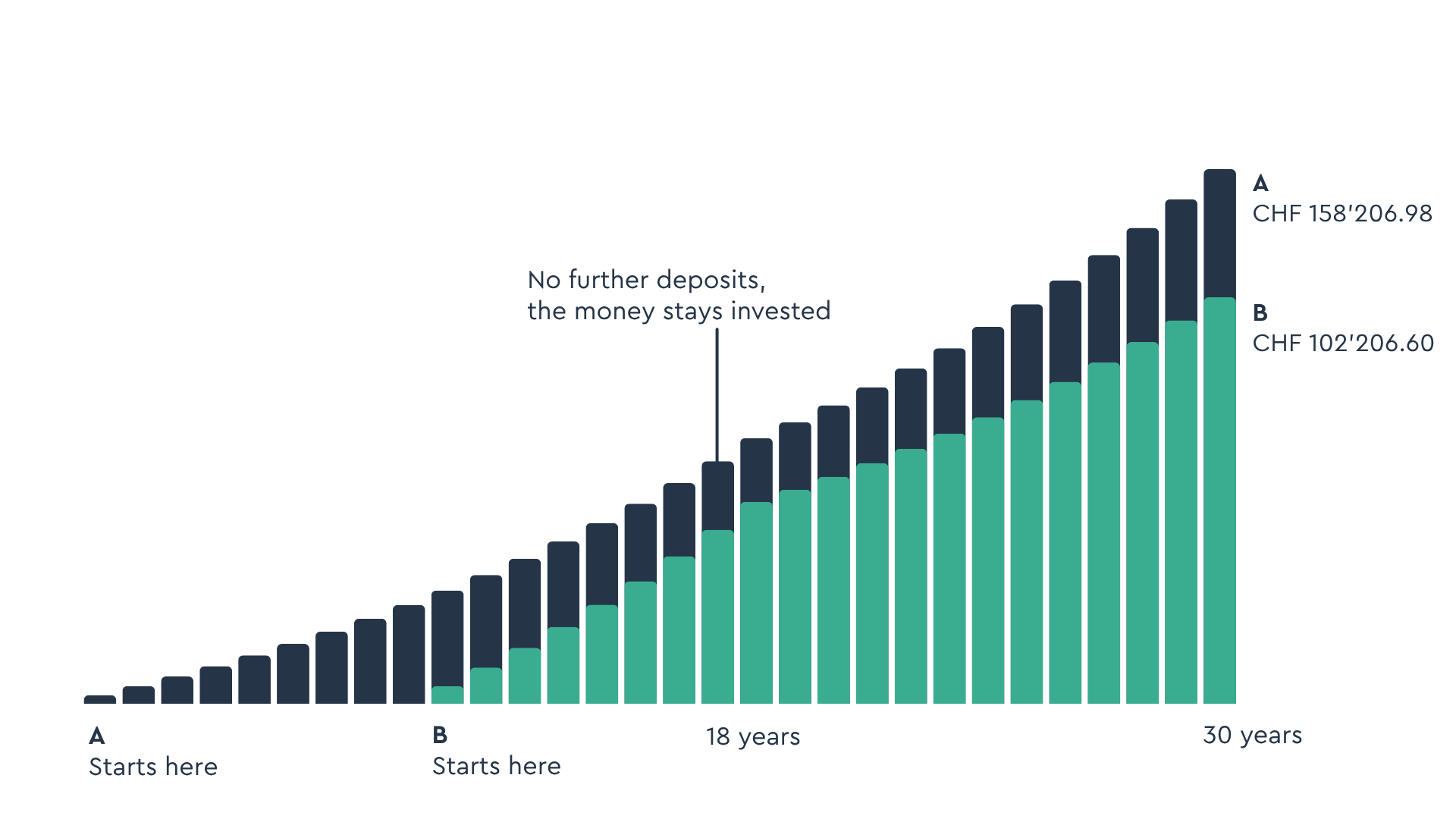

If the children were to leave the money until their 30th birthday (and make no further deposits), Person A’s child would have CHF 158’206.89 and Person B’s child would have CHF 102’942.60 in the portfolio.

How much does the VIAC Invest kids portfolio cost?

The gift portfolio has the same low fees as a conventional portfolio at VIAC Invest.

The total costs consist of the management fee and product costs.

-

-

- The management fee is an all-in fee of only 0.25% of your invested assets. It covers brokerage (transactions), custody fees, foreign exchange, and the actual management.

- The product costs (TER) vary between 0.09% and 0.27% depending on the standard strategy you choose. Here, too, no costs are incurred on non-invested money. You can find the exact total costs of the individual strategies under Strategies.

-

Advantages of the VIAC Invest kids portfolio

-

-

- Affordable: At VIAC, you get digital asset management at the best price!

- Broadly diversified: With our passive strategies, you easily invest in thousands of stocks – starting from just 1 CHF.

- Simple: You don’t have to be a financial expert. During onboarding, you will find the right strategy for your investment horizon and risk tolerance thanks to a short questionnaire.

- Completely digital: Everything runs via the app. You skip the paperwork and the trip to a bank advisor.

-

Index Funds vs. ETFs in a kids portfolio

VIAC Invest relies on index funds instead of ETFs. This saves you, for example, stamp duties of up to 0.15% per trade. The reason for this is that with index funds, the actual shares are always subscribed or redeemed (primary transaction), rather than a secondary transaction as with ETFs, on which stamp duty is incurred.

In addition, index funds always trade at net asset value, and there is no spread (difference between the buying and selling price on the stock exchange).

Who owns the money in a kids portfolio?

The gift portfolio belongs to the person who opens it. This means you remain the beneficial owner of the assets. This allows you to stay flexible. You can save for your child and freely dispose of the money at any time. This way, you can decide for yourself when to gift the assets to the child or whether to convert them back into your own portfolio.

Should the client relationship run through me or directly through the child?

| Advantages | Disadvantages |

| No matter how your life situation changes (for example, in case of divorce or insolvency): The money belongs to the child. | No flexibility in handling the money: If you change your mind later about the use of the money, you can no longer access it – the decision is final. |

| Advantages | Disadvantages |

| If you change your mind about the use or experience a financial bottleneck, you can access the money at any time. This means you decide when or if you want to gift the money to the child. | For the transfer, your child must create their own VIAC account. At VIAC, this is quick and easy and, above all, completely free. |

| Creating a VIAC Invest account only takes a few minutes. If you already have an account, no further documents are required to create a kids portfolio. | |

| Godparents or grandparents of the child can also open a kids portfolio. |

Who is a kids portfolio suitable for?

The gift portfolio at VIAC Invest is particularly suitable for:

-

-

- Parents who want to build wealth for their children early on

- People who want to save regularly with small (or larger) amounts

- People who are not stock market experts and want to invest easily

- Long-term oriented investors with a clear investment horizon

- Anyone looking for a simple “set-and-forget” solution

-

Kids portfolio compared to other solutions

Savings Account vs. ETF Savings Plan with a Broker vs. VIAC Invest Kids Portfolio

| Savings account at a bank | ETF savings plan | VIAC Invest |

| No rebalancing | Usually no rebalancing | VIAC Autopilot takes care of rebalancing on its own |

| No return (low interest), inflation reduces purchasing power | Return opportunity | Return opportunity |

| No financial knowledge necessary | More personal responsibility, basic financial knowledge necessary | Very simple through the onboarding process. You don’t have to be a financial expert. |

| Free | Often inexpensive | Cost-effective |

Comparison of kids portfolios from different digital providers

*Based on assets of CHF 30’000, fully invested in a global strategy

| VIAC | Finpension | Findependent | True Wealth | Selma | |

| Administration and product fees | 0.46% | 0.47–0.49% | 0.52–0.65% | 0.65% | 0.68% |

| Stamp duty | 0.00% | 0.00%-0.30%1 | 0.00%-0.30%1 | 0.00%-0.30%1 | 0.00%-0.30%1 |

| FX markups | Included | Included | 0.50% | 0.10% | 0.25% |

| Minimum deposit in CHF | 1 | 1 | 500 | 1’000 | 2’000 |

| Child’s assets? | No | No | No | Yes | No |

| Index Funds/ETFs | Index Funds | ETFs | ETFs | ETFs | ETFs |

1 Purchase and sale of ETFs are subject to stamp duty of up to 0.30% in total.

You can also find the costs of other providers in this comparison by the online comparison service Moneyland.

Disclaimer

There is no guarantee that investing will result in profits. Investing involves risks that you must be aware of. Past performance is not an indicator of future results. This article does not constitute investment advice. Although VIAC has carefully researched the contents and information provided above, their accuracy and completeness cannot be guaranteed. Any liability is declined.