You will find the following information in this article:

-

-

-

- Requirements and rules for a retroactive purchase

- Good to know

- How do I apply for a retroactive purchase into pillar 3a?

- Why it is worth closing gaps in your private retirement provision

- Purchasing into pillar 3a explained with a simple example

-

-

Various conditions and rules apply to closing contribution gaps in private pension provision (i.e. purchases into Pillar 3a):

- The regulations only apply to pension gaps from 2025 onwards, i.e. pension gaps that arose before 2025 cannot be closed.

- There must have been an income subject to AHV contributions in the year in question.

- The maximum amount must already have been contributed in the year in which the retroactive contribution is made.

- Only one retroactive contribution per gap year.

- Only gaps that are not older than 10 years can still be closed.

- The amount of retroactive contributions is limited: In a given year, no more than the maximum amount can be contributed to fill gaps.

- If the account holder makes a withdrawal due to old age, purchases are no longer permitted.

Good to know

Contribution gaps from different years can be combined and closed.

But be careful: if the gaps exceed the maximum annual amount that can be repaid, the “excess” expires and can no longer be repaid in a future contribution year. So combining gaps should be carefully considered to avoid amounts that can no longer be repaid.

Why is it not possible to fill gaps before 2025?

In future, the information needed to check the requirements must be passed on when switching providers. As this was previously not the case, it is not possible to check whether the conditions for the years prior to 2025 apply and therefore whether an retroactive contribution may be made.

How do I apply for a retroactive purchase into pillar 3a at VIAC?

Retroactive purchases will be integrated directly into the app and you can submit an application for a purchase directly to VIAC at the earliest possible date (01.01.2026).

Why it’s worth making retroactive contributions to pillar 3a:

Retroactive contributions are worthwhile as they can be deducted from taxes just like ‘normal’ contributions to private retirement provision. For people with gaps in their retirement provision, it is therefore a win-win: they close their gaps and save on taxes at the same time.

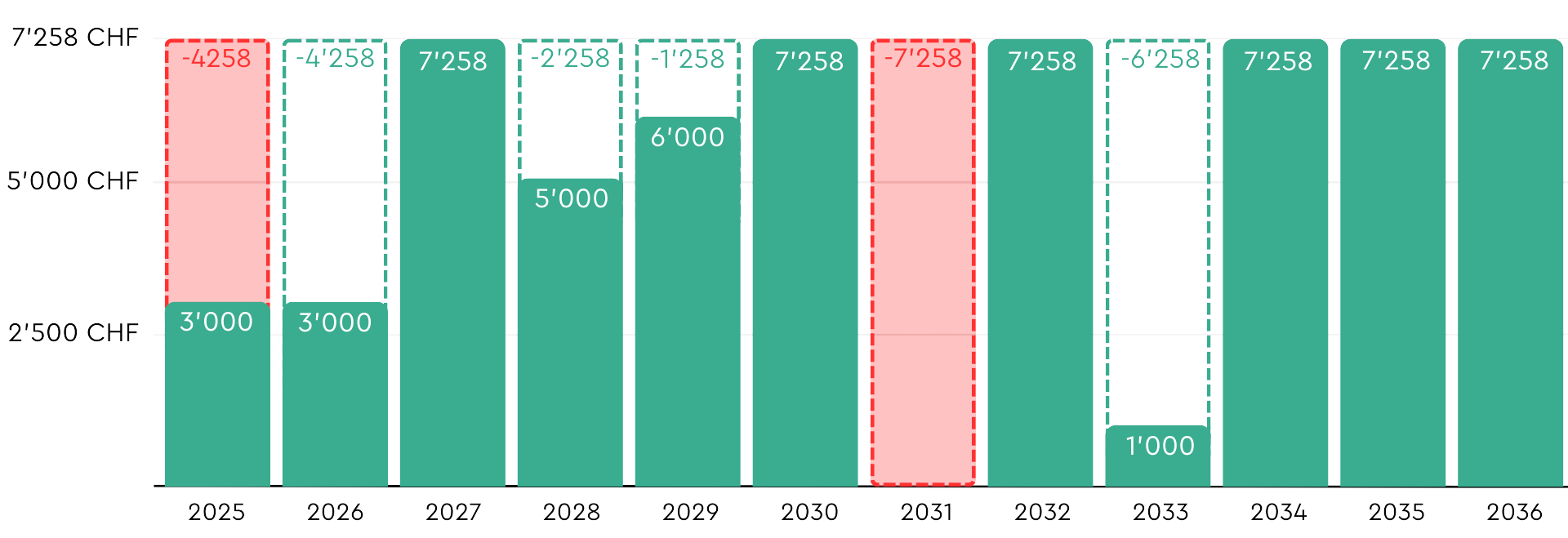

The purchase into pillar 3a explained with a simple example

Preliminary remark: To simplify the example, we calculate each year with the same 3a maximum amount of 7’258.- (according to the year 2025).

The year is 2036.

Viktor has been working since 2024 and earned income subject to AHV contributions. In 2031 he went sailing around the world for 1 year (during which he did not work).

These are his deposits into pillar 3a since 2025:

Viktor therefore has gaps in 2025, 2026, 2028, 2029, 2031 and 2033.

In the current year 2036, Viktor has already deposited the maximum amount in pillar 3a and can therefore now close gaps from previous years.

The gap in 2025 is already over 10 years old and can therefore no longer be closed. Viktor cannot close the gap in 2031 either, as he did not earn any income subject to AHV contributions in that year. These two gaps will exist forever. All other gaps are not older than 10 years and can therefore still be closed.

As the gap from 2026 can no longer be closed next year (i.e. in 2037), he decides to close it this year. This gap is only 4’258 CHF and since it does not yet reach the maximum amount that can be retroactively contributed each year (i.e. the maximum pillar 3a amount), he can close another gap. He opts for the 2028 gap.

4’258 + 2’258 = 6’516.

He therefore contributes an additional 6’516 CHF to his pillar 3a in order to close the gaps for 2026 and 2028.

For next year, Viktor plans to close the gaps for 2029 and 2033. To do this, he must of course first deposit the maximum annual amount into his pillar 3a for 2037. He notices that the two gaps for 2029 and 2033 total 7’516 CHF. This is higher than the annual maximum amount (7516-7258=258 CHF). If he closes these gaps together, he will lose the gap of 258 CHF and will never be able to close it again, as only one payment per gap year is permitted.

He therefore decides to close only the 2029 gap next year and plans to close the 2033 gap the year after (2038).

Conclusion: Although the 3a purchase involves a little complexity, we offer you a simple & digital way so that you can always get the most out of your pillar 3a!